Internal Audit Checklist – Part C – Review & Reporting – I

Part C – Review & Reporting - I

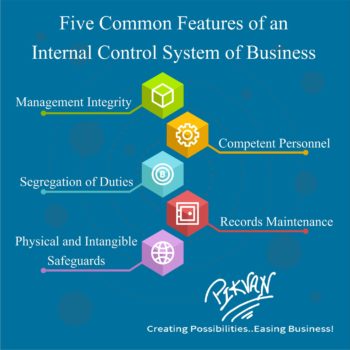

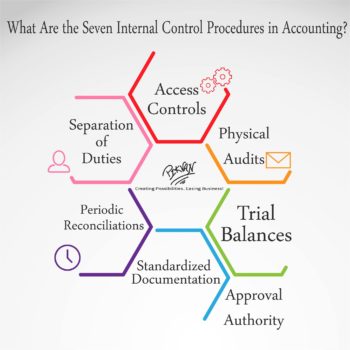

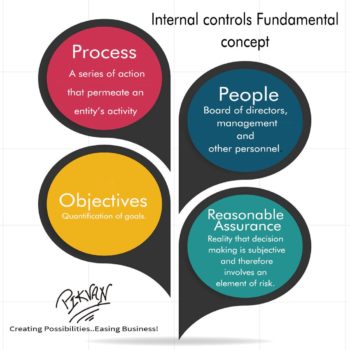

Internal Control System

“The process designed, implemented and maintained by those charged with governance, management and other personnel to provide reasonable assurance about the achievement of an entity’s objectives with regards to the reliability of financial reporting, effectiveness and efficiency of operations, safeguarding of assets and compliance with applicable laws and regulations.

Pre-Requisites for Internal Control Systems –

- Organizational Objectives

- Organizational Structure

- Operating Policies

- Standard Operating Procedure

- Planning and Budgeting: Make a detailed budget and plan of action and it should be compared with the actual & variance. The budget should be practical and achievable.

- Management Information System: Effective Management Information System (MIS) is a time tested technique for controlling various activities.

- Informal Grapevine: The management should listen to informal feedbacks carefully, verify the correctness and reliability of the information and then accordingly should take action.

- Internal Audit: It is one of the best techniques to monitor and control various business operations.

- Management Personnel: High integrity and Ethical values and committed to diligently perform key internal control procedures.

- Boards of Governance: It should have more “hands-on” oversight involvement in the entity’s activities. Entity-level controls such as inspecting and approving supporting documentation.

- Key Controls: Reviews of accounting systems reports, inspections of supporting documents for certain selected transactions, overseeing periodic counts of inventories and reviewing bank statements and other reconciliations.

- IT System: IT system limits risks of errors or fraud and can produce better and more accurate financial reports.

- Monitoring Control Activities: Management should be performing daily “walk-around” controls that provide feedback on the effectiveness of accounting, internal control and operational systems.

- Maximization of Effectiveness & Efficiency: It can be done by including activities that are tailored to the nature, size and complexity of the entity. Management personnel will communicate internal controls through frequent contact with accounting personnel.