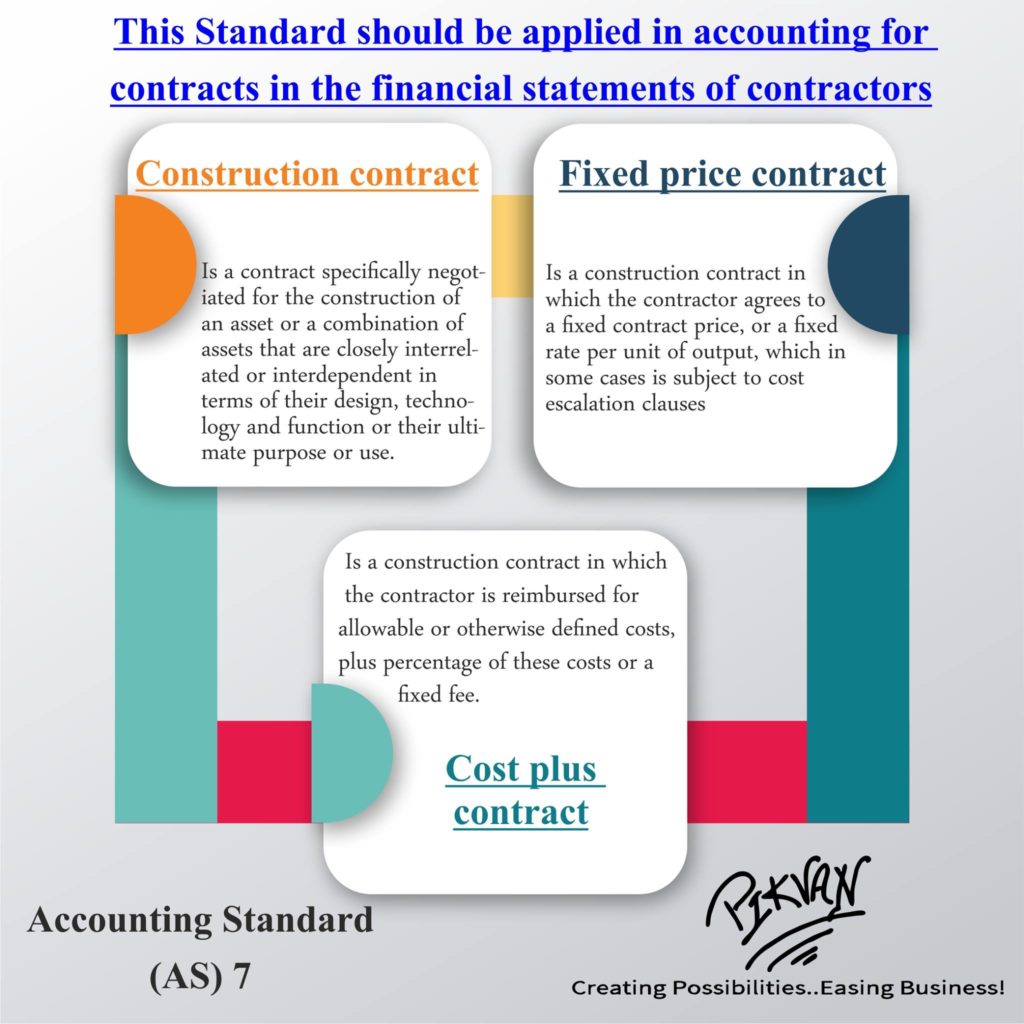

The objective of this Standard is to prescribe the accounting treatment of revenue and costs associated with contracts. Because of the nature of the activity undertaken in contracts, the date at which the contracting activity is entered into and the date when the activity is completed usually, fall into different accounting periods.