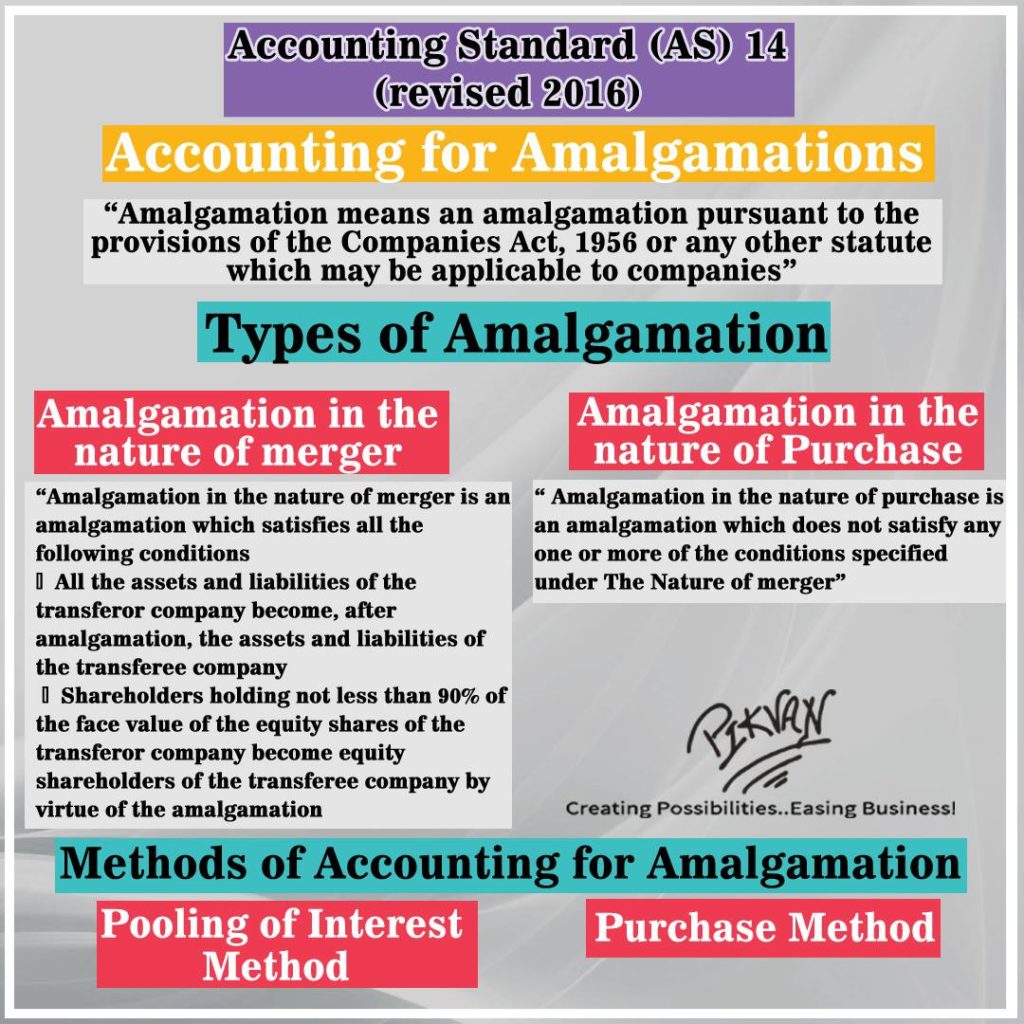

This standard deals with accounting for amalgamations and the treatment of any resultant goodwill or reserves. This Standard is directed principally to companies although some of its requirements also apply to financial statements of other enterprises.