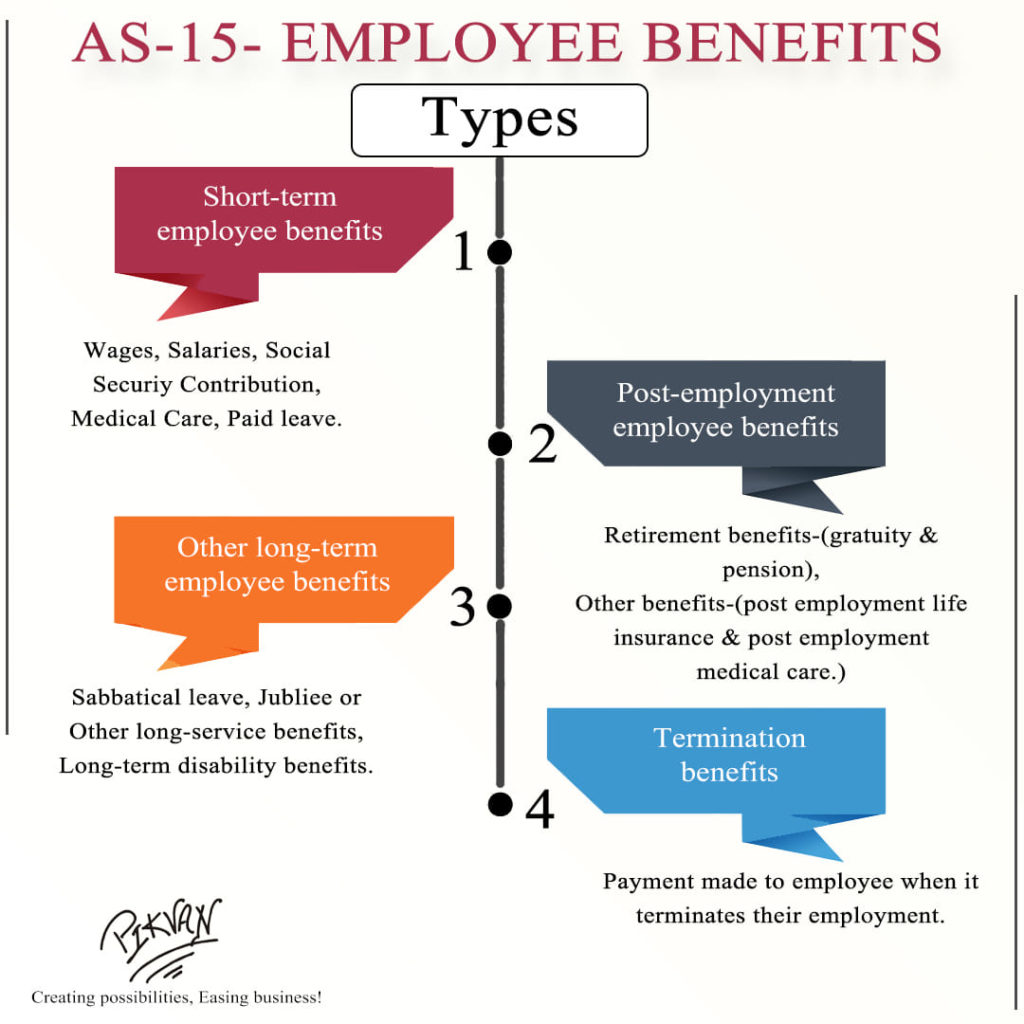

The objective of this Standard is to prescribe the accounting and disclosure for employee benefits. The Standard requires an enterprise to recognise: (a) a liability when an employee has provided service in exchange for employee benefits to be paid in the future; and (b) an expense when the enterprise consumes the economic benefit arising from service provided by an employee in exchange for employee benefits.