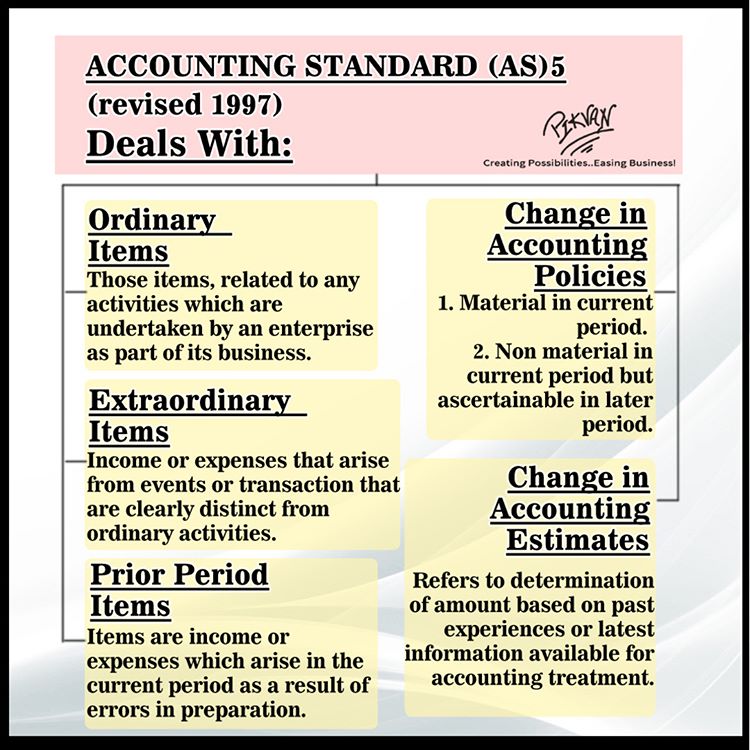

This Standard should be applied by an enterprise in presenting profit or loss from ordinary activities, extraordinary items and prior period items in the statement of profit and loss, in accounting for changes in accounting estimates, and in disclosure of changes in accounting policies.