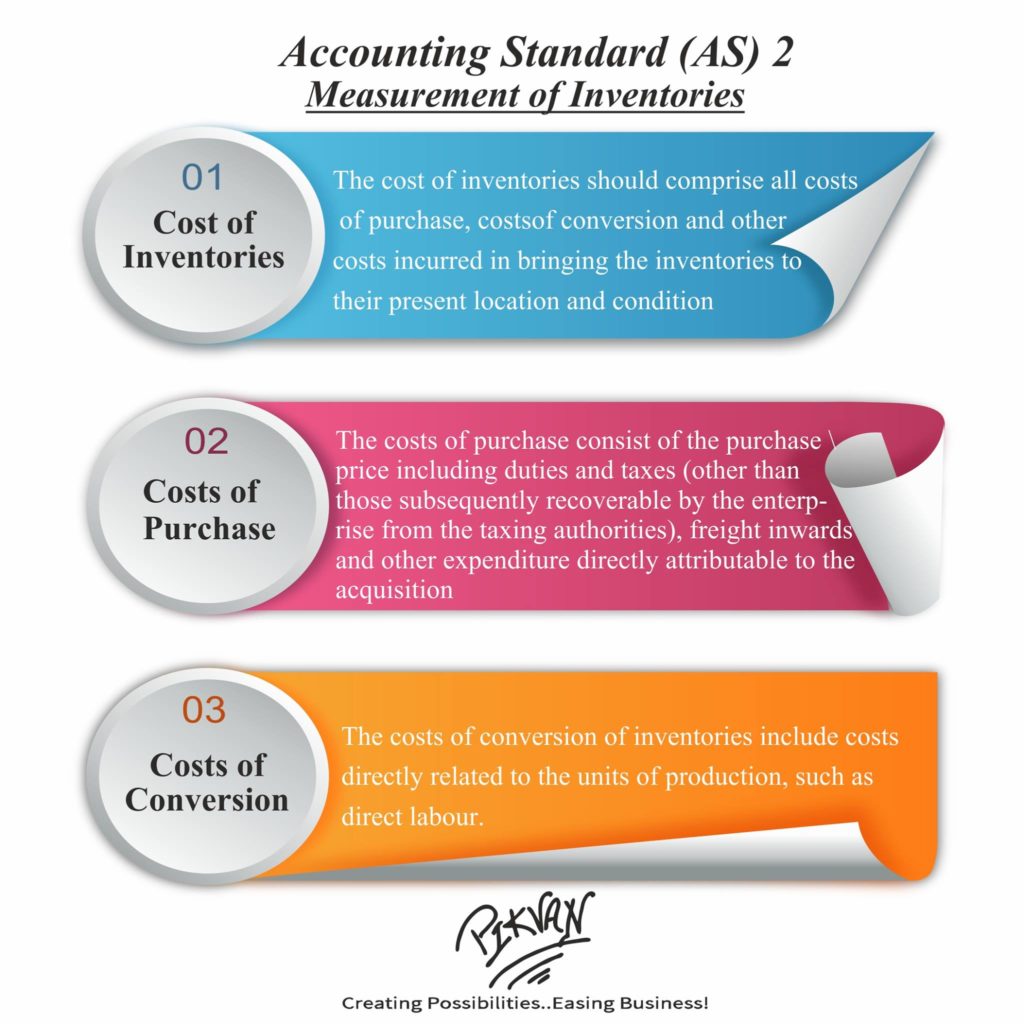

A primary issue in accounting for inventories is the determination of the value at which inventories are carried in the financial statements until the related revenues are recognised. This Standard deals with the determination of such value, including the ascertainment of cost of inventories and any write-down thereof to net realisable value. Inventories should be valued at the lower of cost and net realisable value.